Canadian Housing Outlook: Testing the Basis

11 min read

Query 1: It is well-known that Canadian housing markets are softening as borrowing prices have jumped. How can we choose the depth of the correction up to now?

Within the second quarter, Canadian residence gross sales declined by 20% on a quarter-on-quarter foundation, whereas nationwide common residence costs dropped by 9%. And, nationwide gross sales and costs took one other leg down in July. Nonetheless, peeling away the headline reveals a extra nuanced regional story (Chart 1):

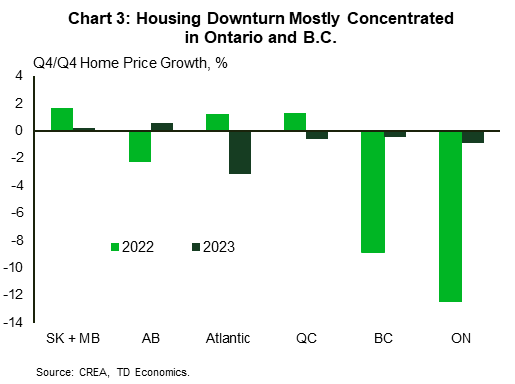

- Dwelling costs have fallen by probably the most in Ontario and B.C. – two markets which noticed speedy affordability deteriorations in the course of the pandemic. What’s extra, elevated investor demand in Ontario left it extra susceptible to a correction.

- Costs have additionally fallen at a comparatively steep clip in Alberta, though gross sales ranges are nonetheless fairly wholesome and markets are comparatively tight, so circumstances look stable in comparison with B.C. and Ontario. Elsewhere, Quebec additionally noticed a significant deterioration in affordability within the pandemic. As such, the moderation in value progress up to now means that the correction in costs nonetheless has legs.

- The story is totally different elsewhere within the nation. In the remainder of the Prairies and the Atlantic Area, costs are holding up higher. The previous has been supported by among the finest affordability circumstances within the nation, whereas the latter area is drawing assist from strong inhabitants progress and comparatively tight circumstances.

- These differing dynamics seize a partial unwinding of purchaser behaviour in the course of the pandemic. Distant work and the need for bigger dwelling areas prompted consumers to bypass bigger city centres for close by suburbs or exurbs. Some selected to find even additional away (whereas some left their residence province all collectively). These behavioural shifts brought about a shock wave to cost progress in markets additional afield to the bigger centres inside B.C. and Ontario, that’s now deflating sooner than within the main markets.

- To have this dynamic happen concurrently throughout giant provinces is irregular. In B.C., for instance, this sample of outsized changes in markets outdoors of the GVA has held true in prior housing downturns. Nonetheless, this hasn’t usually been the case in Ontario, as costs have sometimes corrected by extra within the GTA than in different less-densely populated jurisdictions within the province.

Relatedly, benchmark costs (that are a much less risky measure than common residence costs) for single-detached houses have dropped 7% since February, whereas rental costs have held up higher. This displays the steeper erosion in affordability for indifferent models in the course of the pandemic. It’s also just like the 2017-2019 expertise, the place a number of macroprudential measures (i.e., Ontario’s Truthful Housing Plan, B-20) and rising rates of interest cooled indifferent markets following their steep affordability deterioration, whereas rental costs elevated.

Not like the 2017-2019 interval, we predict that rental costs will drop in coming months though seemingly not the identical extent (or maybe period) as their single-detached counterparts. Up to now, we have already seen some softening as they’ve declined in 3 of the previous 4 months. Word that rental affordability additionally worsened considerably in the course of the pandemic. As well as, rising borrowing prices and falling costs could possibly be weighing on investor demand for these models, as they’re offering some counterbalance to quickly rising rents.

Query 2: How deep will the correction be and the way lengthy will it final?

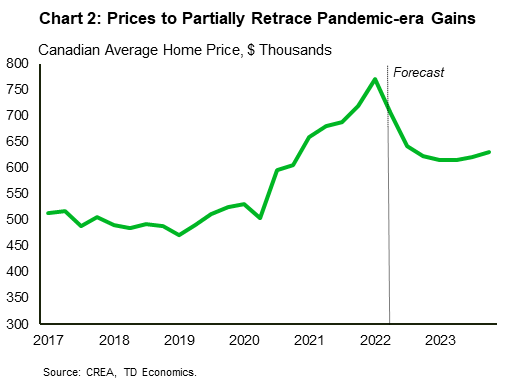

Canadian common residence costs may fall 20-25% on a peak-to-trough foundation from 2022Q1 – 2023Q1 (Chart 2), as gross sales crater by about 35% over the identical interval. Reflecting their affordability deteriorations (Chart 3), steeper declines are forecast in B.C and Ontario whereas extra middle-of-the-road retrenchments are seemingly in Alberta, Quebec, and the Atlantic Area. In the meantime, we count on costs to carry up higher in Manitoba and Saskatchewan over this era.

Our forecasted decline in nationwide residence costs would solely partially retrace the 46% runup over the course of the pandemic. As such, our forecast might be extra aptly described as a recalibration of the market, as an alternative of one thing extra extreme.

Word that our forecasted peak-to-trough decline in Word Word that our forecasted peak-to-trough decline in Canadian residence gross sales falls properly inside the vary seen in previous housing downturns and was surpassed by the World Monetary Disaster, the place gross sales tumbled by 38%. Our projected value drop represents an unprecedented decline (no less than from the late 80’s onwards, when the information started). Nonetheless, it follows an equally unprecedented runup in the course of the pandemic.

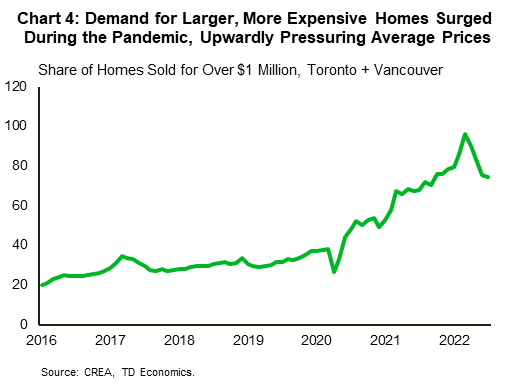

As beforehand famous, demand for bigger, dearer housing soared in the course of the pandemic (Chart 4), which imparted much more upward strain on common residence costs. Due to how they’re calculated, common residence costs are disproportionately impacted by transactions that happen on the higher (or decrease) finish of the worth spectrum. This has now switched from being a tailwind to a headwind for common costs, as valuations for dearer models (like indifferent housing) are unwinding at a comparatively speedy tempo.

Query 3: Why a “recalibration” and nothing worse?

We predict there are some elements that may assist cushion housing demand and costs:

- Firstly, following the quickest price hike cycle in many years, we count on the Financial institution of Canada to pause its climbing marketing campaign within the fourth quarter or, no less than, transfer in a lot smaller increments thereafter. That will place the majority of tightening within the coverage price behind us. Secondly, we count on 5-year bond yields

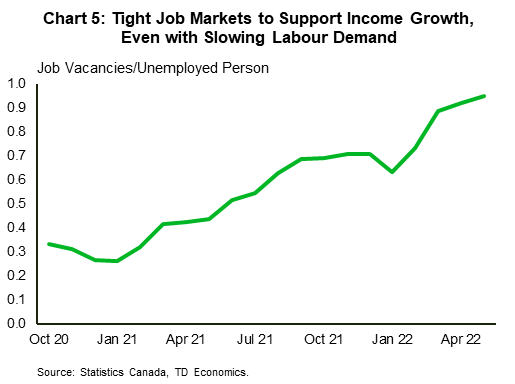

(which underpin 5-year fastened mortgage charges) to dip subsequent yr as financial exercise softens and inflation slows. And at last, it is vital to remember the fact that mortgage qualification stress exams in Canada had been explicitly designed to qualify consumers at a lot greater charges than what prevailed via a lot of the pandemic. This has added a layer of safety from rising charges for each debtors and lenders that’s missing in lots of international locations additionally experiencing an rate of interest shock, like the USA. - Our baseline forecast captures a soft-landing situation the place private revenue continues to develop. Furthermore, labour markets are presently extraordinarily tight and a few slowdown in labour demand may serve to revive steadiness (Chart 5).

- Canadian shoppers have constructed a pool of extra financial savings, which seems to be to have elevated within the first quarter on the again of sturdy progress in worker compensation. It is a key distinction from previous cycles, even within the occasion of recession. The weird pool of financial savings affords an extended lifeline to finance present mortgages and down funds as decrease costs entice consumers again.

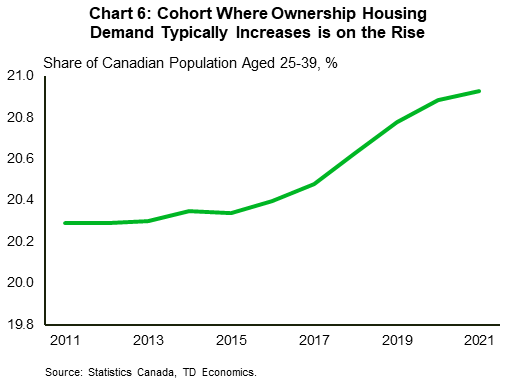

- Inhabitants and demographic elements are demand-supportive. Canadian inhabitants progress is strong, providing basic assist to demand (significantly within the Atlantic Area), whereas the share of Canadians getting old into cohorts the place possession housing demand sometimes will increase can be on the rise (Chart 6).

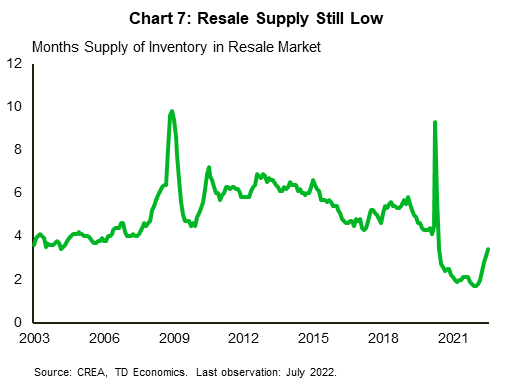

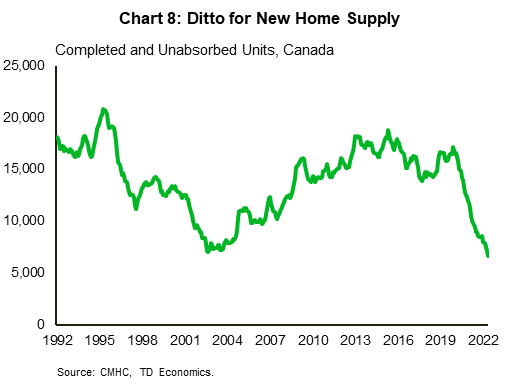

- Stock ranges in each the brand new and resale markets are low. Even because it’s hooked greater not too long ago, the months’ provide of resale houses remains to be properly beneath long-run norms, whereas the share of standing stock within the new residence market stays traditionally low (Charts 7 and eight). A big a part of it is a consequence of the previous cyclical power in demand. Nonetheless, structural elements, like an getting old inhabitants (which tends to maneuver much less) and lengthening development timelines proceed to carry down provide.

Query 4: What’s your longer-term view of the market?

Lengthy-term, we’re extra constructive on the outlook for housing. This has to do with our view that inhabitants progress ought to stay wholesome, underpinning basic demand for housing. Word that the federal authorities is concentrating on 432k new everlasting residents in Canada this yr. A lot of this quota is being stuffed by individuals who’re seemingly already within the nation and are transitioning from non-permanent to everlasting resident standing. Information from Immigration, Refugees and Citizenship Canada signifies that in a typical yr, these transitions account for about 25% of latest everlasting residents, though this determine is nearer to 50% in 2022. Nonetheless, for those who web these folks out, immigration this yr is on monitor to match 2017’s stable degree, which was throughout Canada’s most up-to-date inhabitants growth.

Their targets for 2023 and 2024 are much more formidable in comparison with 2022, as they’re concentrating on some 450k new everlasting residents in Canada in each years. Traditionally, the federal government has seen combined outcomes on this entrance, with the variety of new everlasting residents falling beneath goal in some years and exceeding it in others.

After subsequent yr, we estimate that to simply sustain with inhabitants progress (and different drivers of basic demand), Canada would require about 215-220k new models every year via 2028, which is considerably above the nation’s pre-pandemic run-rate for begins. Nonetheless, that is solely a part of the story. With rates of interest rising and residential costs prone to solely partially retrace pandemic-era positive factors, affordability ought to stay strained over the subsequent a number of years. So, the restoration stage of the cycle is prone to replicate a slower value progress pattern than the previous decade, the place Canadian common residence costs rose at annual common tempo of seven%.

Query 5: What about housing’s influence on the general financial system?

Our forecast anticipates that the housing downturn will shave from 1 – 1.5 ppts from GDP from 2022Q2 – 2023Q1 as residential funding declines and shopper spending is hit by falling residence costs. It is a milder hit to progress than what happened in the course of the World Monetary Disaster and the late-80s housing downturn. On the identical time, it is extra according to what happened in the course of the mid-90s and is extra extreme than the policy-induced decline in exercise noticed from 2017-2019. It additionally is not sufficient, in our baseline forecast, to trigger a contraction in general GDP.

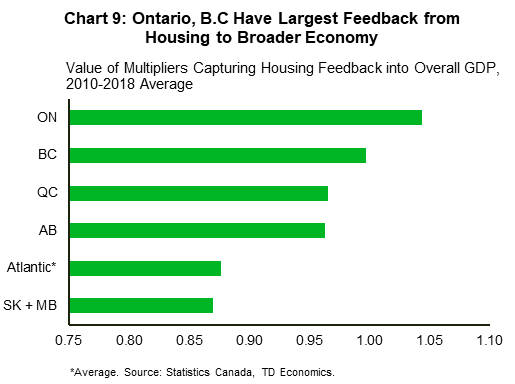

Regionally, the impacts of the housing downturn are seemingly going to be felt extra in B.C. and Ontario. Housing ought to retrench probably the most in these two markets and their general economies have traditionally been extra delicate to spillovers from housing (Chart 9). On the other finish, there needs to be much less spillover in Saskatchewan, Manitoba and the Atlantic Area as housing ought to maintain up higher, and the historic linkages between housing and the remainder of the financial system aren’t as pronounced.

Query 6: What are the dangers or particular concerns on your outlook?

There are a number of:

- The most important draw back threat stems from a steeper and/or extra protracted financial slowdown than our baseline. Our prevailing base case assumes barely constructive progress and solely a reasonable enhance within the unemployment price from its present 4.9% degree. This raises the prospect that the housing correction spills extra broadly into the general financial system, exacerbating financial weak spot and making a unfavourable suggestions loop.

- In a current report, we sketched out how a recession may play out in Canada (see right here). The thought is that progress may sluggish greater than anticipated within the second half of this yr, earlier than contracting mildly via a lot of 2023. Such a situation would generate extra upward strain on unemployment charges with knock-on results to housing demand. Nonetheless, so long as the financial downturn was shallow, costs would in all probability hold a few of their pandemic-era positive factors, particularly as an financial contraction would finally permit policymakers to decrease rates of interest if inflationary pressures likewise come down sooner.

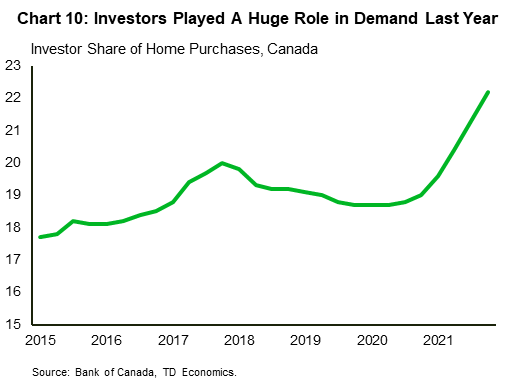

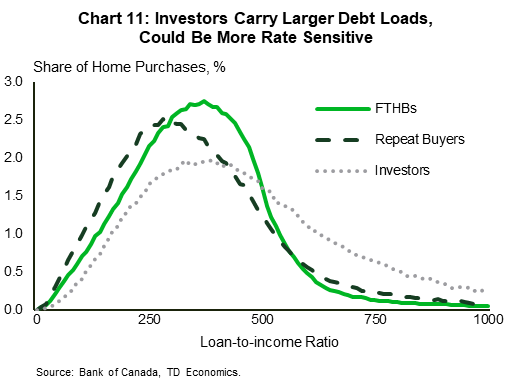

- Traders performed an outsized position in housing demand in 2021, and sure via the early a part of this yr (Chart 10). Nonetheless, some portion of the contraction we’re seeing now might be would-be traders remaining on the sidelines as housing cools, particularly as these consumers are seemingly extra interest-rate delicate (Chart 11). It is attainable that this supply of demand sours greater than anticipated.

- On the availability facet, it is also attainable that listings rise sooner on the upper carrying prices. This is able to imply extra provide and decrease costs for a given degree of demand, and could possibly be very true for traders, who are inclined to have greater loan-to-income ratios. The Financial institution of Canada estimates that solely 2% of Canadian households have variable price mortgages with variable funds (i.e.,householders which are instantly impacted by rising borrowing prices). Nonetheless, this nonetheless quantities to round 300k households. Word that Canadian new listings have but to interrupt meaningfully greater since housing started its recalibration.

- It is also logical to imagine that financial weak spot may trigger a lift in provide as folks lose their jobs and are pressured to checklist their houses. Nonetheless, notice that new listings fell, on common, within the two recessions previous to the pandemic. In different phrases, a supply-side shock is much less prone to unfold independently as a result of as famous earlier, Canada’s stock of houses just isn’t in extra to inhabitants dynamics. A requirement-side shock could be the extra seemingly wrongdoer, thereby exacerbating provide because of a sooner retreat in consumers relative to sellers.

- Federal authorities insurance policies have combined influences and are unlikely to sway housing outcomes an excessive amount of. As an example, the overseas shopping for ban (set to start out subsequent January), is unlikely to hit demand an excessive amount of, given the various cohorts which are exempt from it, and the truth that overseas shopping for taxes are already in place in B.C. and Ontario. In distinction, the anti-flipping tax on residential properties may have some influence on demand, though information gaps make any potential influence troublesome to quantify. In the meantime, the First Time Dwelling Financial savings Account ought to assist first-time homebuying demand, though it is capped at solely 40K, whereas the Housing Accelerator Fund ought to enhance provide, albeit with a lag. Furthermore, the federal authorities’s goal of 100k new houses by 2024-25 via the Accelerator Fund is unlikely to maneuver the needle an excessive amount of on affordability.

Disclaimer

This report is offered by TD Economics. It’s for informational and academic functions solely as of the date of writing, and is probably not acceptable for different functions. The views and opinions expressed might change at any time primarily based on market or different circumstances and should not come to move. This materials just isn’t meant to be relied upon as funding recommendation or suggestions, doesn’t represent a solicitation to purchase or promote securities and shouldn’t be thought-about particular authorized, funding or tax recommendation. The report doesn’t present materials details about the enterprise and affairs of TD Financial institution Group and the members of TD Economics should not spokespersons for TD Financial institution Group with respect to its enterprise and affairs. The knowledge contained on this report has been drawn from sources believed to be dependable, however just isn’t assured to be correct or full. This report accommodates financial evaluation and views, together with about future financial and monetary markets efficiency. These are primarily based on sure assumptions and different elements, and are topic to inherent dangers and uncertainties. The precise consequence could also be materially totally different. The Toronto-Dominion Financial institution and its associates and associated entities that comprise the TD Financial institution Group should not answerable for any errors or omissions within the info, evaluation or views contained on this report, or for any loss or injury suffered.